Your Medicare Situation

Click on your situation below — we'll show you exactly what you need to know.

CALL NOW

You're turning 65 — and the clock is already ticking. Medicare won't wait for you to figure it out.

Click Here to Learn More

You're leaving your work coverage — don't wait until your last day to start planning. By then, it's almost too late.

Click Here to Learn More

Most people who stay on work coverage after 65 are making a big mistake. There are usually much better options.

Click Here to Learn More

You're losing or gaining Medicaid — and that changes everything about your Medicare. Don't get caught off guard.

Click Here to Learn More

Your FEHB premiums keep going up — and more federal employees are finding out they have better, cheaper options. Are you overpaying?

Click Here to Learn More

You're a state teacher or school employee — and you have options nobody's told you about. It's time to look.

Click Here to Learn More

You've got TRICARE — great coverage. But you could be saving thousands a year on your Part B premium and not even know it.

Click Here to Learn More

If you use the VA, you could get money back on your Part B premium every month — and still keep your VA care. Most veterans have no idea.

Click Here to Learn More

You're retiring from OPERS — and Medicare just got complicated. Don't make a decision until you know where you stand.

Click Here to Learn MoreTurning 65

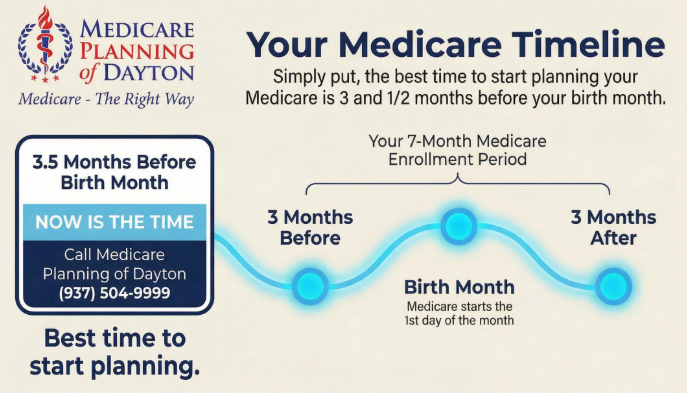

You're about to go on Medicare — and if you're like most people, nobody's told you that you're already on a timeline.

Your Medicare Timeline

We call it your Medicare Timeline, and it's the single most important thing to understand before you turn 65. Your enrollment window opens 3 months before your birth month and closes 3 months after. That's 7 months — and every month matters.

Miss your Medicare Timeline, and you could face penalties and gaps in coverage that follow you for years.

Don't Wait Until the Last Minute

Most people don't start planning until it's almost too late. Your Medicare Timeline says you should start 3 and a half months before you turn 65. Not the week before. Not the month of. The earlier you start, the more options you have.

- First, you need your Medicare card. If you're already collecting Social Security, your card comes automatically. If you're not collecting Social Security, you have to sign up for Medicare yourself — and it takes about a month to get that card in hand.

- Then there's the paperwork. Your Medicare supplement or plan application needs to be submitted at least 4 weeks before your effective date.

- Your start date.

Your Medicare always starts on the first of your birth month — unless your birthday falls on the first, then it starts the month before.

We Manage the Timeline for You

That's a lot of moving pieces on a tight timeline. We sit down with you, walk you through your Medicare Timeline step by step, and make sure everything is done right and on time. There's no cost to you for our help, and we work with every major carrier.

Don't try to figure this out on your own. You don't have to.

Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

Leaving Work Coverage / Retiring

You're retiring, your spouse is retiring, or your employer coverage is ending — and now you need to get on Medicare. This is not something you figure out on your last day of work.

Your Timeline Starts Before You Retire

Your Medicare Timeline starts before your coverage ends. If you already have Medicare Part A, you'll need to add Part B — and that takes time. If you don't have Medicare at all yet, there's even more to do.

The 63-Day Rule

Here's what most people don't know: once you lose your employer coverage, you only have 63 days to get your Medicare coverage in place. Miss that window, and you could face penalties or a gap in coverage right when you need it most. We've seen it happen, and it's completely avoidable.

No Gaps. No Surprises. No Scrambling.

That's why you don't wait until your last day. We'll make sure your Medicare plan is in place before your employer/spouse coverage ends — so the day that coverage stops, you're already covered.

Got an HSA?

If you're over the age of 65 and getting ready to go on Medicare, and you've been contributing to a Health Savings Account, you need to stop contributions 6 months before you go on Medicare.

A lot of people miss this, and it can come with tax penalties. We always recommend talking to your tax advisor about the details — but the important thing is knowing about it now, not finding out later.

Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

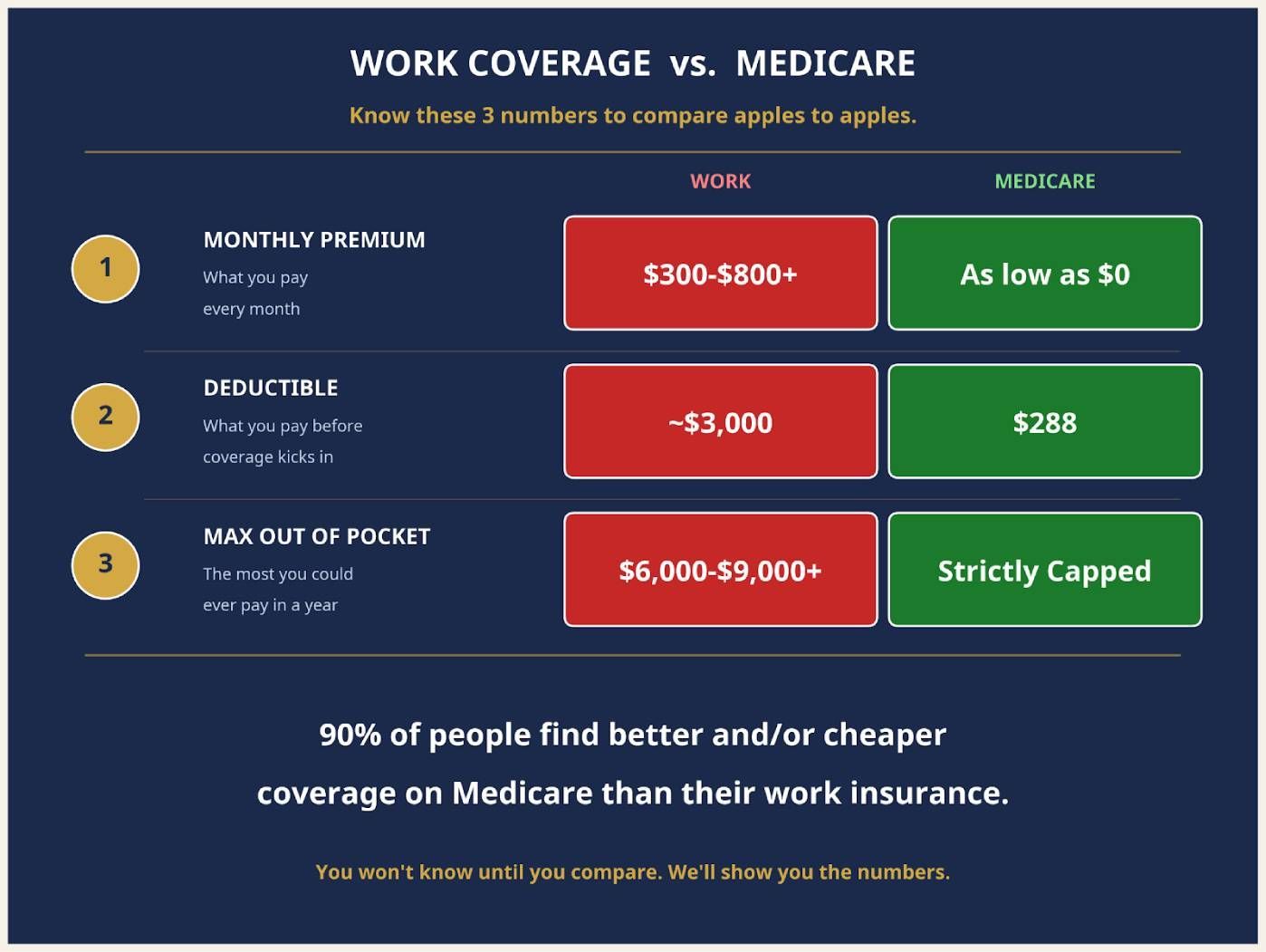

Work Coverage or Medicare?

This is the number one mistake people make after turning 65. They think they have to stay on their employer or spouse coverage. The truth is — you don't.

And 90% of people who compare will find that Medicare is better coverage and costs less.

How to Compare Apples to Apples

When people compare their work coverage to Medicare, they usually only look at one thing: the monthly premium. But that's only part of the story.

To get a true apples-to-apples comparison, you have to look at three specific numbers. If you miss even one of these, you aren't seeing the full picture of what your healthcare actually costs.

1. Premium: What You Pay Every Month

Your employer might subsidize your premium, making it look like a great deal. But when you add up what comes out of your paycheck every month, plus what your spouse pays if they're on the plan, Medicare is often significantly cheaper.

2. Deductible: What You Pay Before Coverage Kicks In

This is where employer plans really hurt you. The average deductible on employer health insurance is around $3,000 — meaning you pay everything out of pocket until you hit that number. On Medicare? The biggest deductible you'll have is $288.

3. Max Out of Pocket: Your Worst-Case Scenario

If you have a major health event, what's the absolute most you could be billed in a year? Employer plans often have max out-of-pocket limits of $6,000, $8,000, or even more. Medicare plans are strictly regulated to protect you from catastrophic medical bills.

You Won't Know Until You Compare

You won't know the real numbers until you compare — and that's exactly what we do. We sit down with you, look at what you're paying now across all three categories, and show you what Medicare looks like side by side.

No pressure, no sales pitch — just the numbers.

Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

Medicare & Medicaid

If you have both Medicare and Medicaid, you're what we call a "dual eligible" — because you have Medicare and Medicaid together. And that actually puts you in a better position than most people realize.

You May Be Eligible for More Than You Think

Dual eligible plans come with more extra benefits than any other Medicare plan out there. We're talking benefits that go beyond basic healthcare. Depending on how you qualify, you could get a monthly amount for groceries, utilities, over-the-counter items, and more. And most people on Medicare and Medicaid don't even know these plans exist.

If Your Medicaid Status Changes, Your Medicare Has to Change Too

This is the part most people miss — and it has to happen immediately. If you gain Medicaid status and you're already on a Medicare plan, we need to switch you to a dual eligible plan so you're getting every benefit you're entitled to. If you lose Medicaid status while you're on a dual eligible plan, we have to get you off that plan and onto a regular Medicare plan right away.

Don't Wait — Call Us Immediately

As soon as you get notification from the state that your Medicaid status has changed — gaining it or losing it — you need to call us. Do not wait. Do not sit on it. The longer you wait, the bigger the problem gets. We'll look at your doctors, your medications, and find the right plan for your new situation. You don't have to figure this out on your own. Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

Federal Employee Benefits (FEHB)

Your FEHB premiums keep going up year after year — and more federal employees are discovering they can suspend their FEHB, go on Medicare, and save a remarkable amount of money.

You Have Three Options — Most People Only Know About One

As a federal employee, you have three options when it comes to Medicare and your FEHB coverage.

Option 1: Keep FEHB Only

Stay on your federal plan and skip Medicare Part B. No Part B premium, but no help from Medicare either. You can still enroll in Medicare Part A at no cost, even if you keep FEHB.

Option 2: Keep FEHB + Add Medicare

Medicare becomes your primary coverage and works alongside your FEHB to reduce your out-of-pocket costs. The trade-off: you'll pay the Part B premium of $202.90/month on top of your FEHB premium.

Option 3: Suspend FEHB + Go on Medicare Advantage

This is the one most federal employees don't know about — and it's where the real savings are. You suspend your FEHB (never cancel — always suspend), enroll in Medicare Part A and B, and we help you find a $0/month Medicare Advantage plan. No FEHB premiums. Usually lower total costs. Better benefits.

The Safety Net

You can always re-enroll in FEHB during a future Open Season if you ever need it back.

Never Cancel — Always Suspend

Never cancel your FEHB — always suspend. We have the OPM Health Benefits Cancellation/Suspension Confirmation Form right here in our office. We'll walk you through it.

You Won't Know Until You Compare

You won't know which option is best until you compare them side by side — and that's exactly what we do. Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

STRS / SERS

If you're a retired state teacher or school employee going on to Medicare, you have more options than you think — and they're probably better than what the state is offering you.

What Most People Don't Realize

Your retirement healthcare through the state? It's just a Medicare Advantage plan. That's it. It's the exact same type of plan we help people with every single day.The difference is the state plan usually comes with a monthly premium. The plans we can show you? Most of them have no monthly premium at all.

Why Does This Happen?

When large retirement groups have thousands of people, insurance companies come in and create plans specifically for that group. But those plans aren't always built with you in mind — they're built around the numbers. And that means the plan you're being offered through the state may not be the best option available to you.

What We Do

We sit down with you and compare your state retirement options against the regular Medicare options — apples to apples. Same type of plan, side by side. And most of the time, people choose the Medicare options we show them over what the state is offering. When you come in, bring your healthcare brochure from the state. That way we can compare everything right there and you'll see exactly where you stand. Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

TRICARE

If you're under 65, you're on TRICARE Prime. Once you turn 65, you move to TRICARE for Life — and you're required to pick up Medicare Part A and Part B to keep it.

We're Not Here to Talk You Out of TRICARE

We're here to add to it. There are Medicare Advantage plans made specifically for TRICARE beneficiaries — and they don't cost you a dime. Zero monthly premium. You just add it on.

Here's What You Get

- A considerable reduction on your Part B premium every month — potentially saving you thousands of dollars a year

- Extra benefits like gym memberships, dental, and vision

- And because you have TRICARE, you don't need drug coverage — so these plans are built without it

What About Copays?

If for some reason you have a copay on your Medicare Advantage plan, TRICARE will pay it. So you're covered either way.

No Risk

If you ever decide it's not for you, you can cancel anytime with no penalties. You keep your TRICARE for Life. You keep all your benefits. You just add a plan that saves you money and gives you more. Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

VA Benefits

If you use the VA for your healthcare, you may not think you need Medicare at all. A lot of veterans feel that way. But here's what we always recommend:

Pick Up Medicare Part A and Part B During Your Initial 7-Month Window

If you don't, and you need it later, you could face a lifetime penalty.And when has the government ever kept things the same? If the VA makes cuts or changes your benefits, you'll want Medicare as a backup. Don't get caught without it.

It Won't Cost You a Thing

There are Medicare Advantage plans made specifically for VA beneficiaries. Zero monthly premium. You just add it on. These plans can give you a considerable reduction on your Part B premium every month — potentially saving you thousands of dollars a year. They also come with extra benefits like gym memberships, dental, and vision. And because you use the VA, you don't need drug coverage — so these plans are built without it.

It's a Backup Plan When You Need It Most

We've had clients who were traveling and had a heart attack. They weren't near a VA — but because they had their Medicare Advantage plan, they were covered. Or maybe you have a serious condition and you want a second opinion from a doctor outside the VA. Now you have other insurance that lets you do that — and it didn't cost you anything to have it.

No Risk

You keep your VA care. You keep everything you have. You just add a plan that saves you money, gives you a backup, and protects you if anything ever changes. And if you ever decide you don't want it, you can cancel anytime with no penalties. Your Medicare puzzle is different from everyone else's. Don't just get on the plan your neighbor has — their puzzle isn't yours. We put your Medicare puzzle together correctly, finding you the right plan for your personal situation.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.

OPERS

You're retiring from the Ohio Public Employees Retirement System — and Medicare just got complicated. Don't make a decision until you know where you stand.

It All Comes Down to One Number: 20 Years

If you have 20 or more years of qualified health care service credit, you qualify for an HRA — a Health Reimbursement Arrangement through OPERS. That's real money. OPERS deposits funds into your HRA every month to help cover your Medicare costs.

But here's the catch:

To get that money, you have to enroll in your Medicare plan through a company called Via Benefits — and you have to do it over the phone.

We Will Not Enroll You if You Qualify for the HRA

Not because we don't want to help you — but because if we do, you lose your HRA money. And we're not going to do that to you. That would be doing you a disservice, and that's not how we operate.

What We Can Do

We can sit down with you before you call Via and help you understand Medicare — what the parts mean, what to look for, what questions to ask. That way, when you get on the phone, you're not going in blind. You'll know exactly what you're looking at.

If You Have Less Than 20 Years of Service Credit

GOOD NEWS — you don't qualify for an HRA, which means Via Benefits doesn't matter to you. Now you can do Medicare the easy way. Come sit down with us. We do Medicare the right way — face to face. We'll look at your doctors, your medications, and find the right plan for your situation.

Now, Let's Talk About Your Spouse

About 10 years ago, OPERS stopped covering spouses. That means your husband or wife has to get their own Medicare plan.

And they don't have to go through Via Benefits to do it.

Bring your spouse in with you. We'll take care of them right here — face to face — so they don't have to deal with doing it over the phone. There's no cost for that help, and we give them the same lifetime service and support that all of our clients receive.

Call us at (937) 504-9999 or

We never charge for helping you plan your Medicare. That's how it should be.